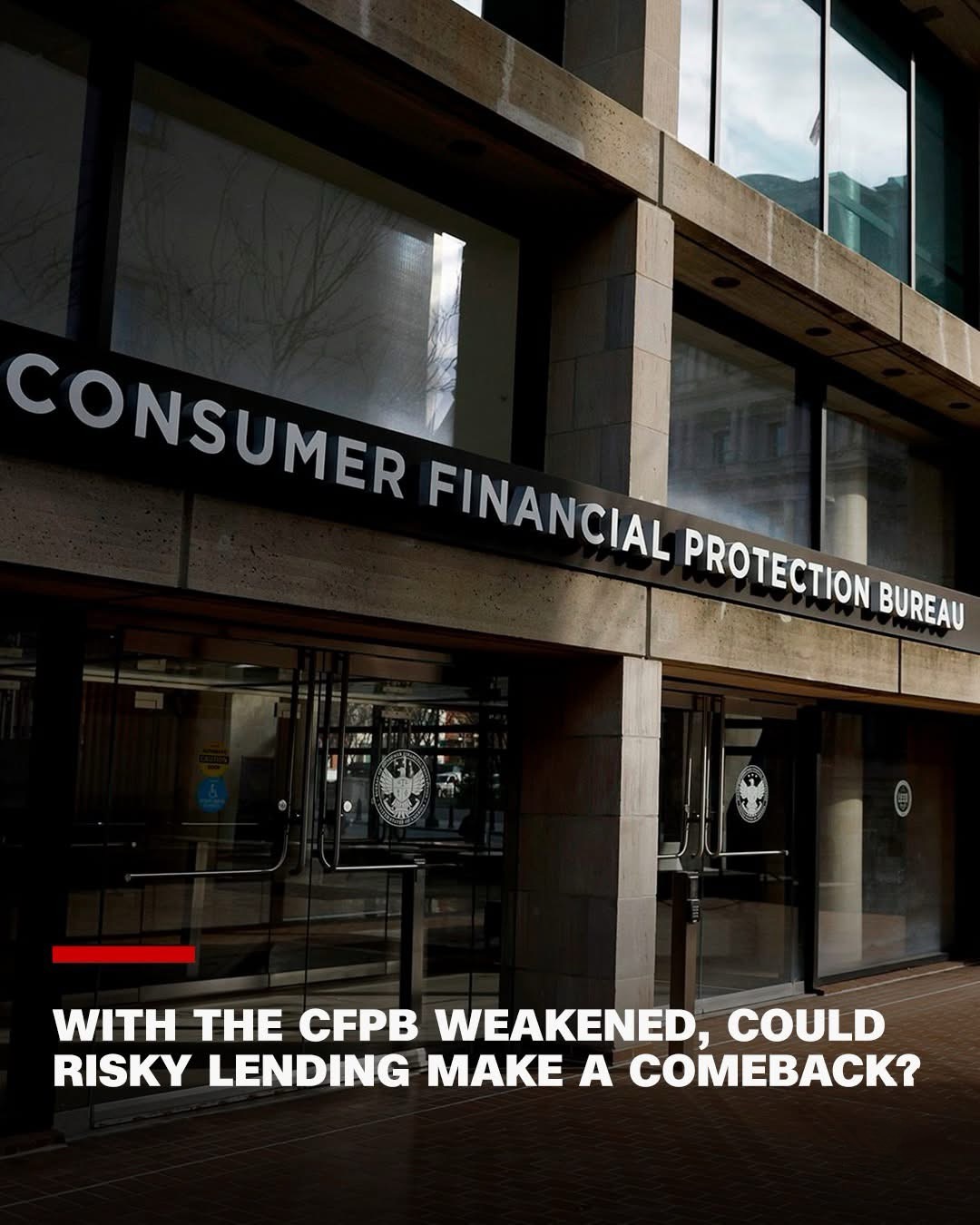

The Consumer Financial Protection Bureau (CFPB), the banking watchdog established in response to the subprime mortgage crisis and the 2008 global financial meltdown, has been thrown into turmoil as the Trump administration moves to sharply curtail its authority.

Last month, CFPB employees were ordered to halt their work, effectively shutting down the agency—though that directive has since been challenged in federal court.

Despite the agency’s weakened state, experts told CNN that Americans are unlikely to see a repeat of the subprime mortgage crisis that led to its creation. Banks and lenders are now subject to stricter regulations, and borrowers benefit from stronger protections than they did before the financial crisis.

However, with the CFPB—an agency designed to serve as a consumer safeguard—effectively sidelined, Americans may need to take a more proactive role in protecting themselves when dealing with lenders.

“The CFPB’s mission is to protect individuals. After the financial crisis, we saw many people who had been taken advantage of,” said John Griffin, a finance professor at The University of Texas at Austin who has argued that widespread fraud contributed to the crisis. “But I don’t think the CFPB alone could prevent another financial crisis.”

The agency was conceived by Democratic Sen. Elizabeth Warren while she was a Harvard Law professor and was established through the Dodd-Frank Act of 2010, a sweeping financial reform law aimed at addressing the vulnerabilities that fueled the crisis. Since its creation, the CFPB has provided $19.7 billion in consumer relief, benefiting approximately 195 million people, according to agency data.

The CFPB did not respond to a request for comment on the impact of its recent changes.

### A Safer Home Loan Market?

For most Americans, buying a home is the largest financial decision they’ll ever make. While understanding mortgage terms has always been crucial, it may become even more important if the CFPB’s influence diminishes.

Despite this, the home loan market is far safer today than it was in the past, said Ira Rheingold, executive director of the National Association of Consumer Advocates.

“When Dodd-Frank passed, it included mortgage reform,” Rheingold said. “The types of loans that fueled the subprime crisis really can’t be made anymore because they would violate the law.”

The 2008 housing meltdown was driven in part by banks and lenders issuing risky home loans to borrowers who couldn’t afford them. These loans were then packaged into complex financial products that collapsed when homeowners started defaulting. The result was a nationwide crash in home prices and millions of foreclosures.

Before 2008, loans requiring little or no proof of income were common. Today, they are rare, said Laurie Goodman, founder of the Housing Finance Policy Center at the Urban Institute.

“Prior to the financial crisis, income wasn’t adequately documented—you sort of took the borrower’s word for it,” she said. “Today, a ‘no doc’ loan would be extremely foreign.”

Since the crisis, laws have strengthened lending standards and improved transparency for borrowers, reducing the likelihood of another collapse.

### What You Should Know

Even so, a weakened CFPB could strip away important consumer protections, said finance professor John Griffin.

“Gutting an organization like the CFPB hurts investors on smaller financial transactions, where they’re more vulnerable to being taken advantage of,” he said. “The CFPB has provided extra scrutiny to address unjust fees and predatory financial practices.”

For homebuyers, this means being extra diligent when borrowing. Carefully reviewing loan terms for hidden fees or conflicts of interest is essential. With mortgage rates hovering just under 7%, borrowers should shop around and compare multiple lenders to secure the best deal.